11

11By Nepali SMM Media Pvt.ltd.

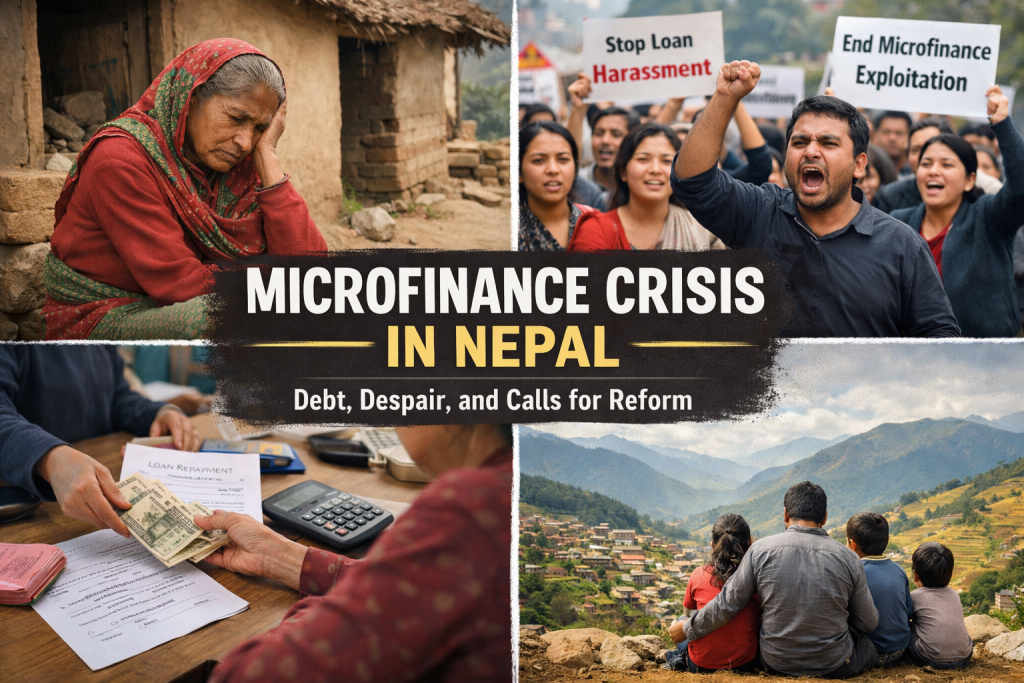

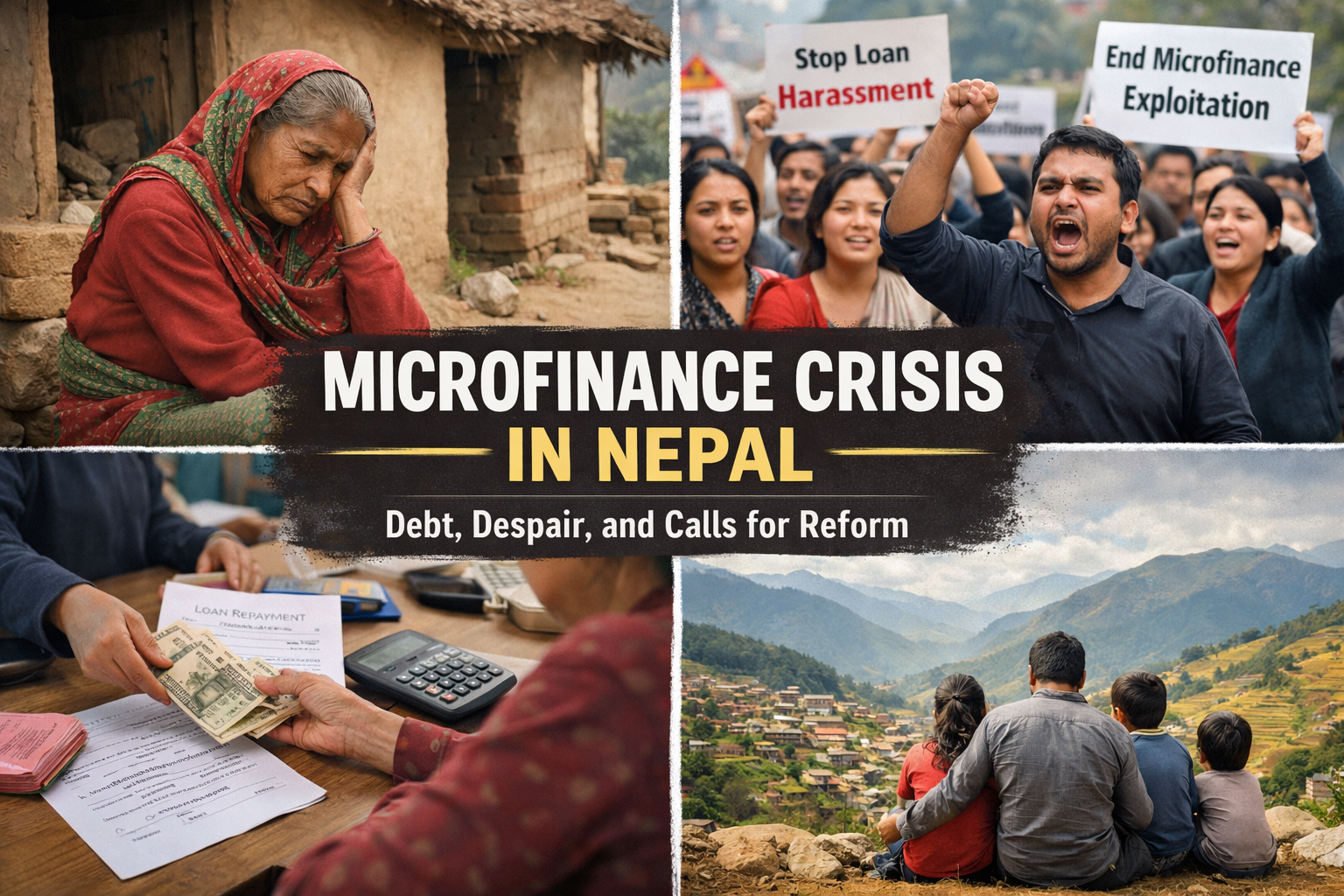

Kathmandu, Nepal — For many Nepalis, access to credit can be the difference between expanding a small business, paying school fees, or coping with an emergency. Over the last two decades, both commercial banks and microfinance institutions (MFIs) have expanded lending to previously underserved communities. Yet this expanded access has brought a growing concern: borrowers increasingly find themselves trapped in cycles of debt, struggling to repay loans and in some cases ending up on credit blacklists that limit their financial future.

This article explores how this situation arises, why it persists, and what experts, regulators, and borrowers themselves say should be done.

In theory, credit is meant to be a tool: it should help individuals start or grow enterprises, smooth income gaps, or meet urgent needs. Microfinance institutions — licensed by the Nepal Rastra Bank (NRB) — were created precisely to offer small, collateral‑free loans to rural and low‑income borrowers who could not access traditional banks.

Similarly, commercial banks have branches across Nepal, offering savings, loans, and other financial services that, ideally, support economic activity.

But the reality many borrowers face is more complex.

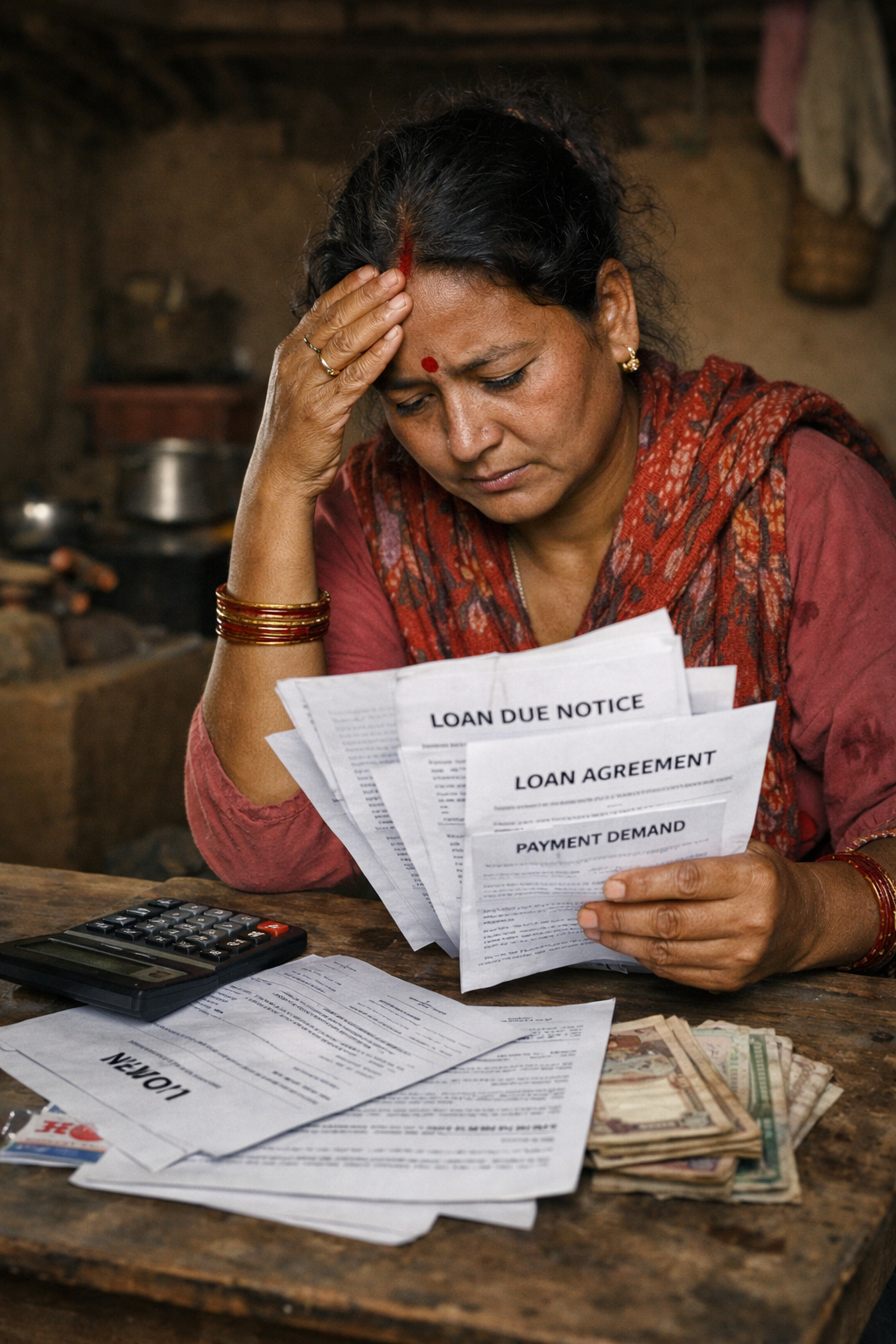

Unlike typical savings deposits where funds are stored securely, loans involve repayment schedules, interest, service charges, and sometimes penalties. When borrowers underestimate future income, or when economic activity slows, meeting these obligations can become difficult.

The term blacklisted refers to a situation where a person’s name is entered into a credit information register maintained by the central bank or a credit bureau. When a borrower misses multiple repayments or defaults on a loan, banks and financial institutions may report them to this registry.

Once blacklisted:

Individuals may be denied new loans

They may face higher borrowing costs

Their financial reputation can be harmed

They can find it harder to conduct business or invest

For individuals striving to improve their economic situation, being on a blacklist can feel like a permanent setback.

One of the main issues driving debt problems is multiple borrowing — when a person takes loans from several institutions at once. A 2023 NRB committee report found that more than 400,000 borrowers had taken loans from two or more institutions, including banks and MFIs. Even well‑intentioned borrowers often do this to repay earlier debts or to meet pressing needs when income is irregular. However, juggling many repayments at different rates can quickly overwhelm families whose incomes are not stable.(fiscalnepal.com)

Borrowers have shared stories — in interviews and on social platforms — of taking additional loans simply to cover earlier payments, creating a cycle of debt that becomes harder to escape.

Nepal Rastra Bank sets maximum interest rates and service charges for microfinance institutions to protect borrowers. Yet even with these caps, borrowers often report that the effective cost of borrowing can feel much higher once additional service charges, insurance fees, and compounded interest are added.

For those with irregular or seasonal income — especially in agricultural areas — a fixed repayment schedule can strain finances during lean months. If borrowers miss a repayment, institutions may charge penalties or report those missed payments to credit registries, pushing borrowers closer to being blacklisted.

The trajectory from one or two missed payments to blacklisting can involve several steps:

Irregular income or shock — illness, loss of employment, market downturn

Missed payments due to cash flow problems

Penalties and added charges on the existing loan

Borrowing from another institution to cover past dues

Reporting of defaults to credit information bureaus

Official blacklisting after repeated defaults

Once blacklisted, borrowers have limited options to refinance or consolidate debt — a challenge both banks and MFIs say they are trying to address through restructuring and rescheduling policies.

Although systematic government data on every aspect of micro‑indebtedness is limited, several credible Nepali media outlets have documented how borrowers experience intense stress when repayment burdens rise.

For example, in a report published by The Kathmandu Post, borrowers described feeling pressure from both MFIs and commercial lenders when they could not meet repayment schedules. Some spoke of their businesses being slow and returns insufficient, leading them to scramble for new loans just to catch up on installments.(kathmandupost.com)

These narratives don’t allege wrongdoing by all institutions, but they do reflect a recurring theme: a mismatch between repayment expectations and real household income — especially when unforeseen events occur.

Acknowledging these challenges, the Nepal Rastra Bank and the Government of Nepal have taken several steps:

The central bank has tightened oversight on MFIs and directed that:

Borrowers should not be allowed to take multiple overlapping loans from different institutions without proper checks.

Interest rates and allowable charges must be clearly disclosed.

Financial literacy must be improved before loans are issued.(kathmandupost.com)

In March 2024, the government reached an agreement with borrower groups demanding relief from aggressive debt collections. The agreement included:

Caps on effective interest and service fees

Protection against unfair practices

Measures to prevent borrowers from being pushed deeper into debt

The move was widely reported in the Nepali press as recognizing the seriousness of borrower concerns.(english.nepalpress.com)

One of the systemic problems is the lack of a unified and transparent credit reporting system historically accessible to all lenders. Without a comprehensive registry, lenders may not fully know a borrower’s existing obligations, leading to multiple overlapping loans and increased default risk.

Initiatives to improve credit reporting and make information accessible to banks and MFIs are under discussion — a step that regulators and industry professionals widely support.

Experts emphasize that debt problems are often symptoms of deeper economic conditions:

Many loan recipients are in informal sectors with fluctuating incomes.

Rural households depend heavily on agriculture, which can be unpredictable.

Economic shocks, such as the COVID‑19 pandemic, reduced incomes when loan repayments were expected to continue.

Economist Dr. Bishnu Raj Upreti (name used here as an illustrative expert) has highlighted that debt stress often reflects gaps between capacity to repay and economic opportunity, not simply predatory lending. Improving livelihoods and income diversification, he notes, is equally important alongside lending reform.

While credit can be a powerful tool, it needs to be balanced by borrower protection:

Many borrowers take loans without full understanding of repayment obligations or the total cost of borrowing. Financial education programs — both from government agencies and financial institutions — aim to address this gap.

NRB has encouraged banks and MFIs to offer loan restructuring — adjusting repayment schedules based on borrower capacity — rather than simply pushing for enforcement or reporting defaults.

Industry associations for MFIs have pledged to strengthen responsible lending practices, including rigorous checks on borrower debt loads and sustainable repayment plans.

For many Nepalese households, access to credit has unlocked opportunities that were previously out of reach. Microfinance and banking have helped people expand small businesses, pay for education, and manage seasonal needs.

Yet, without proper safeguards, transparent information, and realistic repayment expectations, the same credit can become a source of financial stress and lead to negative outcomes like blacklisting and restricted future access to finance.

The solution requires collaboration:

Borrowers, by improving financial planning and understanding terms

Financial institutions, by adopting responsible and transparent lending

Regulators and government, by ensuring protections, strong oversight, and financial literacy support

Only by addressing all sides of the credit equation can Nepal ensure that access to loans empowers citizens, rather than traps them in unmanageable debt.